If I could ask a couple questions?

Apparently, if I am summarizing well, TFP is the transforming of inputs into outputs that are worth more than the inputs. We can get economic growth by using more inputs or by increasing the number of hours works, but that's not really 'wealth creating'. Whereas TFP seems to be actual wealth creation.

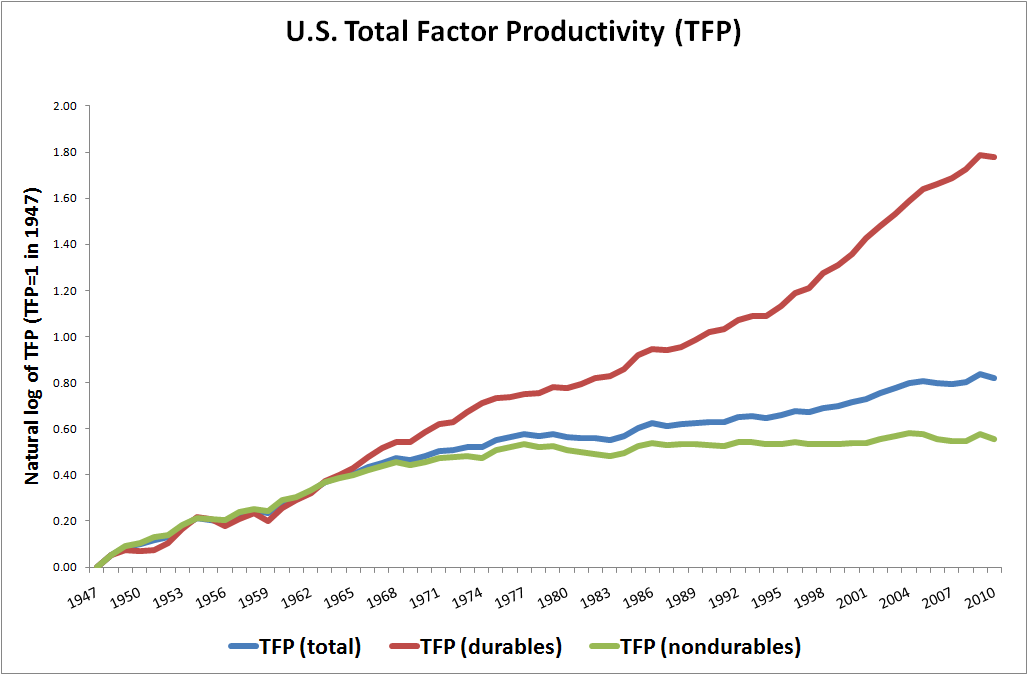

I found this graph.

Nondurable TFP seems to be the economic growth that's generated from innovations and ideas? When people come up with improvements to processes, or ways to improve products so that they're either cheaper or more valuable, is that nondurable TFP?

I think that graph means that the US has only been getting ~0.5% economic growth from 'ideas' for the last few decades. Or at least, that's nearly what nondurable TFP has been. Is there a reason why this stagnation is occurring? My interpretation is that, if we start to stabilise our natural inputs into the economy (population growth and resource extraction), we can only hope for 0.5% economic growth.

As an aside, so many reports on TFP use natural logs, when what I want is % of GDP!

Am I close? Am I using the right graph for what I think it's about?

Apparently, if I am summarizing well, TFP is the transforming of inputs into outputs that are worth more than the inputs. We can get economic growth by using more inputs or by increasing the number of hours works, but that's not really 'wealth creating'. Whereas TFP seems to be actual wealth creation.

I found this graph.

Nondurable TFP seems to be the economic growth that's generated from innovations and ideas? When people come up with improvements to processes, or ways to improve products so that they're either cheaper or more valuable, is that nondurable TFP?

I think that graph means that the US has only been getting ~0.5% economic growth from 'ideas' for the last few decades. Or at least, that's nearly what nondurable TFP has been. Is there a reason why this stagnation is occurring? My interpretation is that, if we start to stabilise our natural inputs into the economy (population growth and resource extraction), we can only hope for 0.5% economic growth.

As an aside, so many reports on TFP use natural logs, when what I want is % of GDP!

Am I close? Am I using the right graph for what I think it's about?

")