You were answered. They didn't understand the problems with the euro and made the mistake of adopting it.

If they didn't understand the problems with the Euro, then the fault still lies with them for agreeing to something they didn't fully understand. Just like if you sign a contract without reading it, you are still bound to honor that contract or pay whatever cost is outlined in the contract to get out of it.

It would have been plenty rational had the EU fixed the euro the moment the flaws were discovered. I.e. it would have been rational for Greece had the EU itself acted rationally. Indeed German policy is not acting rationally. In this regard, if Greece is acting rationally on the assumption that their union partners would act rationally to everyone's mutual interests and somehow that's a fault of Greece, what basis of reasonability are you arguing from that isn't "blame the victim for annoying me"?

How exactly was Greece a victim again? Better yet, what about Greece's actions before joining the EU and during their time in the EU so far could even be vaguely considered rational?

No, Greece is about as much of a victim here as someone who racks up a bunch of credit card debt and then whines about how deep in debt they are. In other words, Greece was a victim of their own irrational and downright irresponsible fiscal policies.

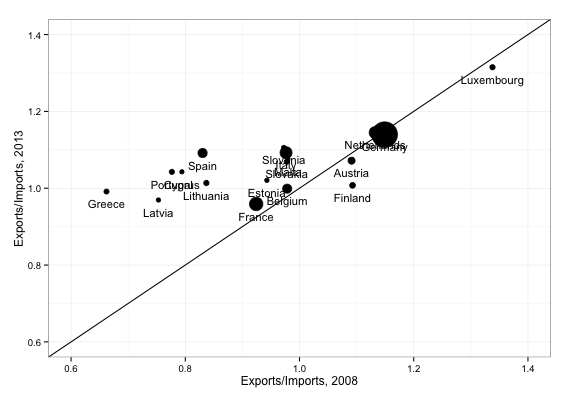

Universal wealth and prosperity was a reasonable outcome if their money was half as efficient as their real economies. But their money is inefficient, with the inefficiencies hurting everyone in the long run but benefiting the top few countries' relative positions against the US (they want our dollars, their cheap euro pushes our firms to buy their stuff with our dollars).

Again, no one is forcing anyone else to participate in the Euro. If these problems are really as bad as the anti-EU crowd are making them out to be, then why don't the smaller nations leave? That is a question neither you nor anyone one else has been able to sufficiently answer. There may not be any official mechanism for leaving the EU or Eurozone, but nor is there any mechanism keeping them in either. So if Germany is taking advantage of other EU members and enacting predatory economic policies, it's because the other EU members are letting them do it. And that is why they are the ones to blame, not Germany. Remember: No one can do anything to you that you don't let them do. So if you are a victim, it's because you made yourself a victim and didn't stand up for yourself.