cegman

Scott Walker Supporter

http://www.freedomworks.org/blog/jborowski/debunking-myths-of-the-great-depression

There are links on the site used to back up the claims

There are links on the site used to back up the claims

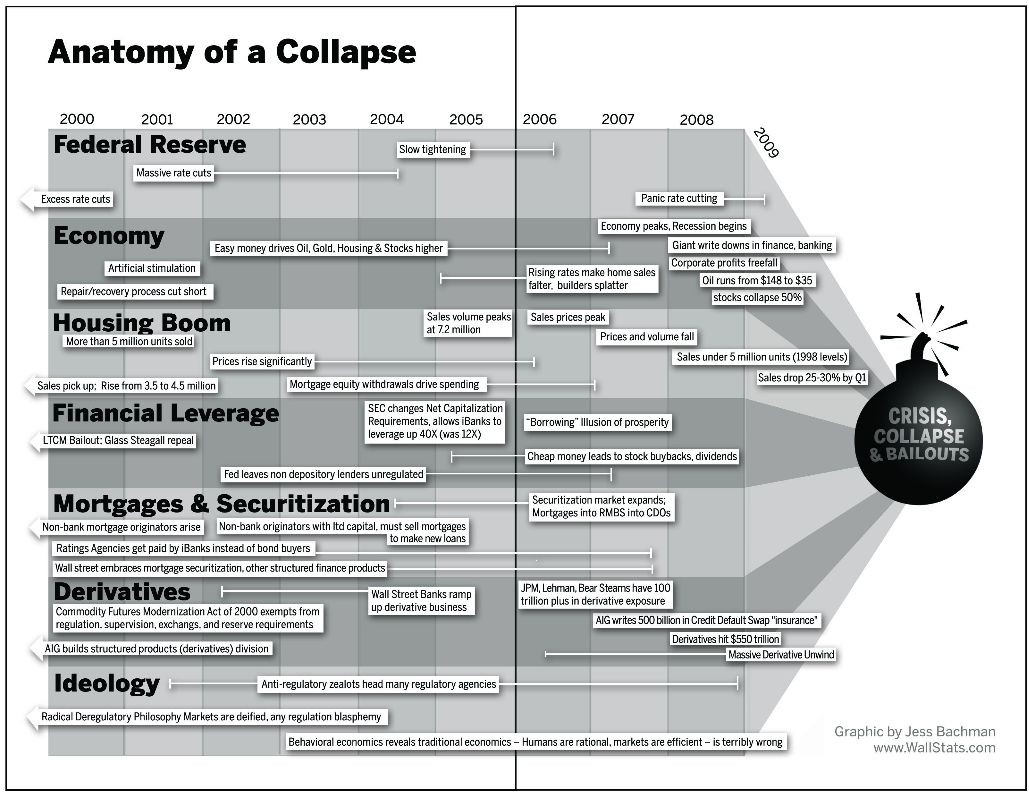

The current economic crisis is often compared to the Great Depression which lasted from 1929 until the early 1940s. From the causes to the policy responses, there are striking similarities between the two economic meltdowns. Unfortunately, the typical high school history teacher continues to perpetuate myths about the Great Depression. Learning the real story of the worst economic crisis in U.S. history is important to stop it from happening again. Listed below are rebuttals to five common myths about the Great Depression.

1. Free Market Capitalism Caused the Great Depression.

Most of us probably learned that “unfettered” and “unregulated” capitalism in the 1920s led to the Great Depression. Some have similarly blamed capitalism for the current economic crisis. But just like today, there was not pure free market capitalism in the 1920s.

The Federal Reserve, the central bank of the United States, was created in 1913. Not only did the Federal Reserve fail to prevent the Great Depression but it was primarily responsible for its length and severity. The Federal Reserve controls the money supply and would never exist in a true free market economy.

As Murray Rothbard explains in America’s Great Depression, the Federal Reserve creates boom and bust cycles that destabilize the economy. The Federal Reserve created an unsustainable boom in the 1920s by lowering interest rates. Rothbard estimated that the money supply had increased by 61.8 percent between 1921 and 1929. The inevitable stock market crash was a symptom of the inflationary boom.

Economist Henry Hazlitt once wrote that “worse than the slump itself may be the public delusion that the slump has been caused, not by the previous inflation, but by the inherent defects of ‘capitalism.’” The blame for the Great Depression should be placed on the Federal Reserve, not free market capitalism.

2. Herbert Hoover Was a Laissez-Faire President.

Many history teachers claim that Herbert Hoover was a “do-nothing” passive president who allowed the Great Depression to happen. Quite the opposite is true. Far from being an advocate of laissez-faire, Hoover was an extremely interventionist president. Hoover actually intervened in the economy more than any prior president.

Herbert Hoover’s interventionist policies prolonged the Great Depression. He doubled federal spending in real terms in just four years. One of Hoover’s first acts as president was to prohibit business leaders from cutting wages. He also launched huge public works projects such as the San Francisco Bay Bridge, Los Angeles Aqueduct, and Hoover Dam. Hoover signed the Smoot-Hawley tariff into law in June 1930 which raised taxes on over 20,000 imported goods to record levels. He raised the top income tax rate from 25 percent to 63 percent and the lowest income tax rate from 1.1 percent to 4 percent in 1932. Despite what most of us have been taught, there was nothing laissez-faire about Hoover.

In the 1932 election, Franklin Delano Roosevelt (FDR) criticized his opponent Hoover of presiding over “the greatest spending administration in peacetime in all of history.”

His statements are seen as a bit hypocritical in hindsight since Roosevelt continued and expanded Hoover’s big government policies. Many of the New Deal programs were based on policies already enacted by the Hoover administration. It could be said that Hoover was the real father of the New Deal.

3. The Federal Reserve’s Tight Monetary Policy Caused the Great Depression.

Federal Reserve Chairman Ben Bernanke and the late Nobel Prize-winning economist Milton Friedman blame the Federal Reserve for the Great Depression. But they do so for the wrong reasons. While Milton Friedman was correct on many economic issues, he was wrong on monetary policy. He was a monetarist who incorrectly believed that the money supply determines the level of economic activity. In his view, an increase in the money supply will lead to more economic activity.

In A Monetary History of the United States, Friedman argued that the economy was strong in the 1920s until the year 1929 when a typical economic downturn occurred. He believed that the economic recession turned into a depression because the Federal Reserve did not print enough money between 1930 and 1933. Friedman and Ben Bernanke essentially blame the Great Depression on the Federal Reserve’s failure to inflate the money supply.

The real problem is that the Federal Reserve inflated the money supply in the 1920’s. Inflationary booms induce widespread malinvestment--bad investment decisions made under the influence of easy money and credit. Malinvestments inevitably lead to wasted capital and economic losses. An economic recession is actually necessary to correct all of the previous malinvestment.

At Milton Friedman’s ninetieth birthday party in 2002, Ben Bernanke even said “I would like to say to Milton and Anna: Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.” He spoke too soon. The current economic situation may not be as severe as the Great Depression—though economists such as Peter Schiff say it could get as bad. But it's clear that the central bank was the main culprit in both financial crises. The Federal Reserve’s expansionary monetary policy in the 1920’s caused the Great Depression, not the central bank’s “tight” monetary policy in the early 1930’s.

4. FDR’s New Deal Ended the Great Depression.

The New Deal is widely perceived to have ended the Great Depression but it actually made the economic situation worse. The series of economic packages implemented between in the 1930s hampered economic growth and prolonged the Great Depression. Roosevelt imposed excise taxes, harmful regulations on businesses, increased the top tax rate to 79 percent, doubled government spending between 1932 and 1940, and artificially raised wages and prices.

The New Deal created many public works projects. Contrary to what most of us were taught, public works projects do not boost the economy. It is the classic case of the seen versus the unseen—we can all visibly see the jobs created by New Deal spending, but it is more difficult to see the jobs destroyed by the high taxes needed to pay for the New Deal programs. Of course, taking money away from entrepreneurs in the private sector will only hurt economic growth.

In 1931, a year before FDR was elected president, the unemployment rate was an unprecedented 16.3 percent. By 1939, nearly two terms into the Roosevelt administration, the unemployment rate had risen to 17.2 percent. The New Deal clearly didn’t lower unemployment like most of us were taught.

In May 1939, Treasury Secretary Henry J. Morgenthau Jr. stated that, “we are spending more than we have ever spent before and it does not work… I say after eight years of this Administration we have just as much unemployment as when we started…And an enormous debt to boot.”

The depression would have been much shorter without the New Deal.